Economic Review: Mar25 – Feb26

A year shaped by shifting interest rates, geopolitical shocks, and diverging market performance

Global Economic Overview

The 2025/26 financial year was defined by three major macro themes

Disinflation → Policy Easing (Early Phase)

Global inflation moderated through much of 2025.

Central banks (including South Africa) began cutting or pausing interest rates.

This supported:

Equity market strength (especially early in the period)

Improved investor sentiment

In South Africa, inflation eased to around ~3–3.6%, allowing rate cuts of ~125bps

Growth Remained Fragile

Global GDP stayed uneven and below trend

South Africa GDP:

Growth ~1%–1.4%

Improvements driven by:

Better electricity supply

Lower inflation

Improved investor sentiment (FATF removal, ratings upgrade)

Geopolitical Shock (Late Phase – 2026)

Middle East conflict (Iran / Strait of Hormuz)

Oil prices surged above $100/bbl

Global inflation risks re-emerged

Markets turned volatile

This created a “second inflation scare”, delaying expected rate cuts globally

South African Economic Themes

Inflation Stability & Policy Credibility

Inflation anchored around ~3%–4%

SARB shifted toward a 3% target

Strengthened policy credibility and investor confidence

Interest Rate Cycle Turning

Rate cuts were supported by consumer relief and asset price stability in 2025

Start of 2026, cuts paused due to global risks

Rand Resilience (with Volatility)

Supported by improved fundamentals and strong commodity exports (Gold)

Pressured by global risk-off periods and USD strength during geopolitical stress

Asset Class & Market Insights

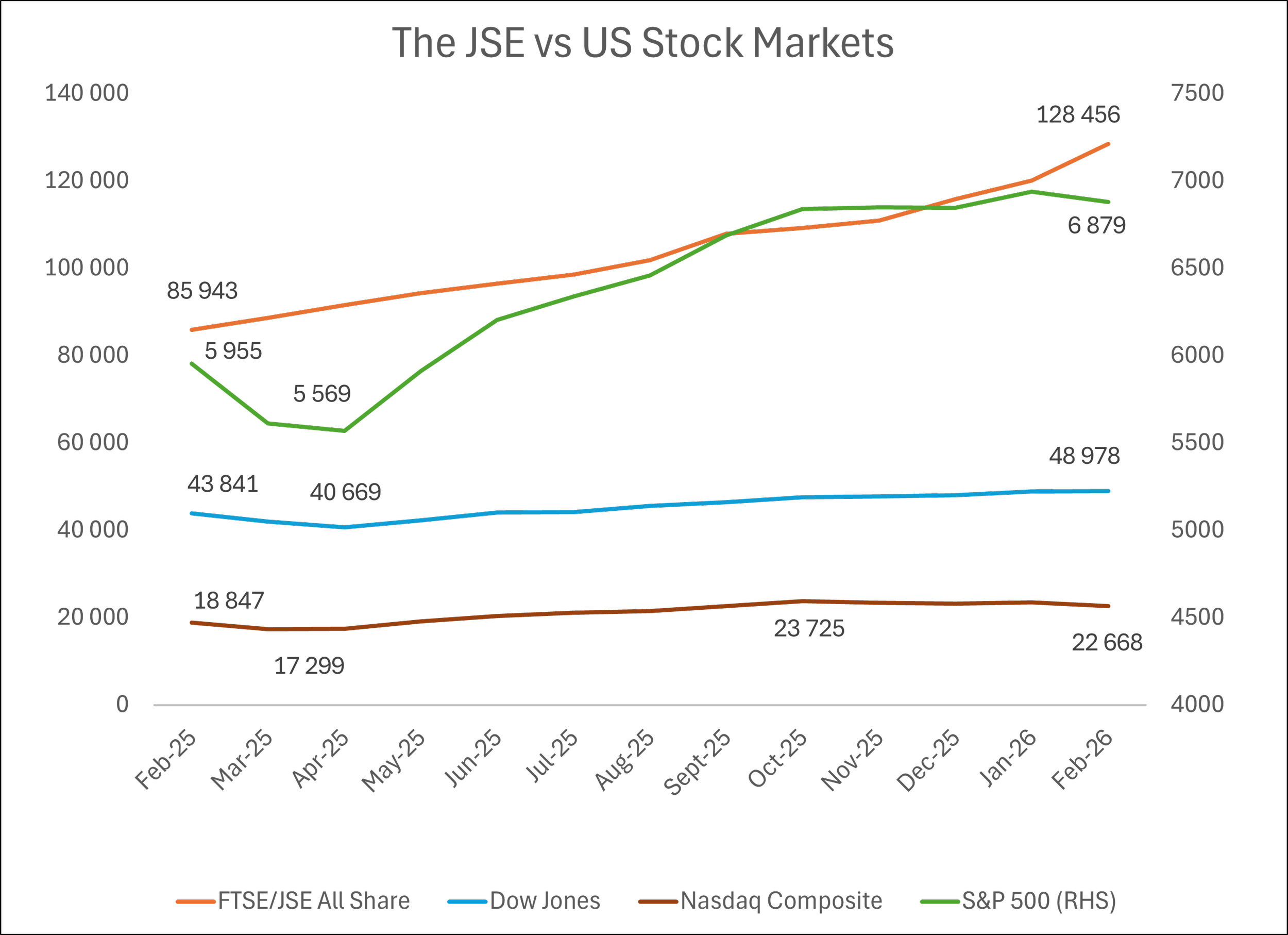

US Markets (S&P 500, Nasdaq, Dow Jones)

Boom → Correction → Volatility

Early period:

Continued momentum from tech/AI optimism

Mid-to-late period:

AI bubble concerns + tariffs triggered sell-off

Significant correction in US equities

Y/Y Growth

S&P 500 +15.52%

Nasdaq +20.27%

Dow Jones +11.72%

US markets showed how quickly sentiment can shift from “growth optimism” to “valuation concern”.

JSE ALSI

Relative resilience

Y/Y Growth +49.47%

Supported by:

Commodity exposure

Stronger Rand (periods)

Improved SA sentiment

SA equities benefited from global diversification and commodity strength, outperforming expectations in a low-growth environment.

The JSE, the Dow Jones and S&P 500 hit their peaks in either January or February 2026, but the Nasdaq Composite hit its high in October 2025

Currency (USD/ZAR)

Volatility within a strengthening trend

Biggest drivers:

Stronger SA fundamentals (positive)

Global risk-off (negative)

USD strength during crises (negative)

The Rand remained a high-beta currency — strengthening in calm markets, weakening during global shocks.

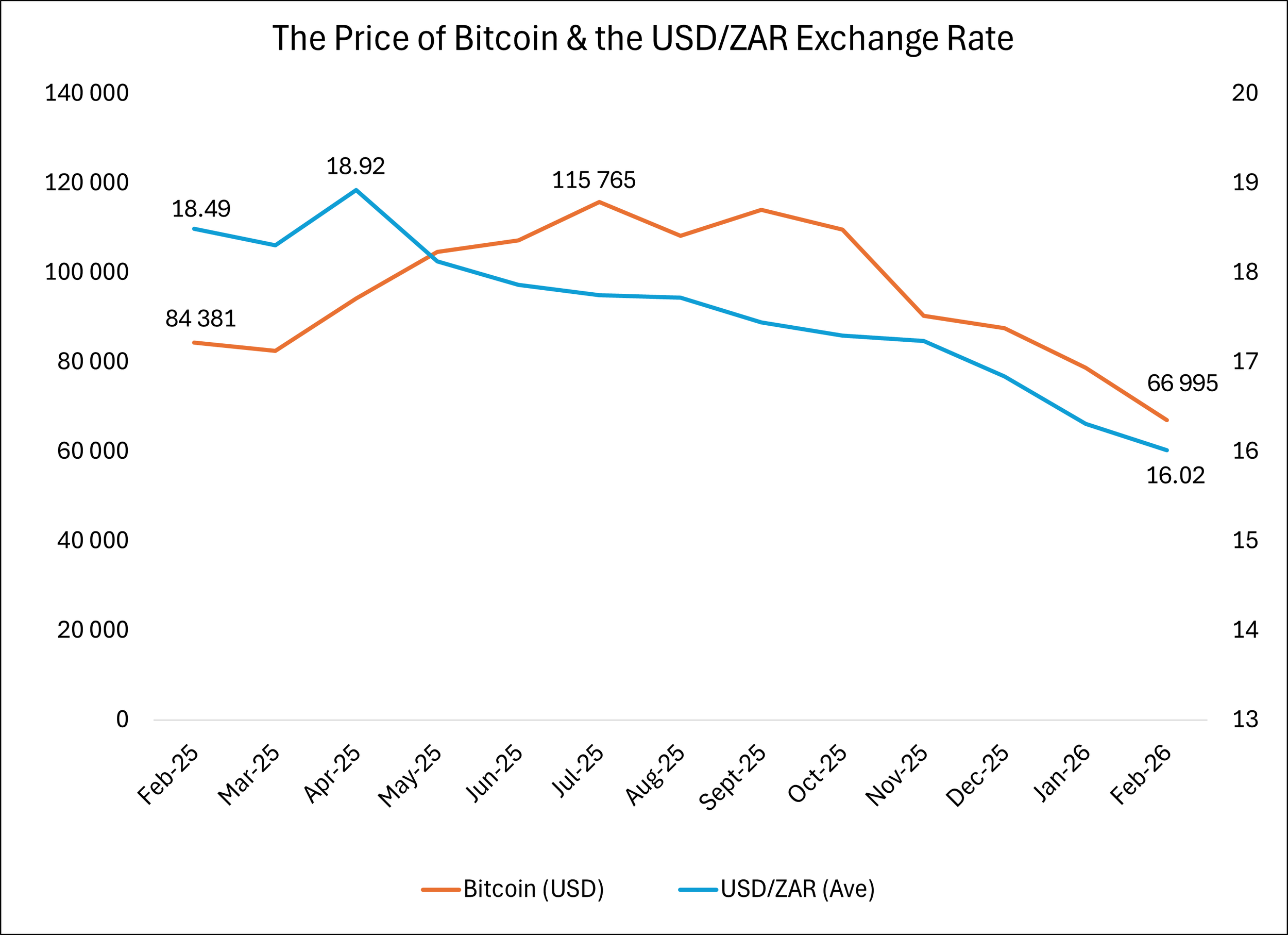

Bitcoin

Institutional adoption vs macro sensitivity

Supported by:

Continued institutional interest

Alternative asset narrative

Pressured by:

Risk-off environments

Liquidity tightening

Bitcoin increasingly trades like a risk asset (tech proxy) rather than a pure hedge (like gold)

Up until February 2026, the rand went from strength to strength, but bitcoin lost momentum after September 2025

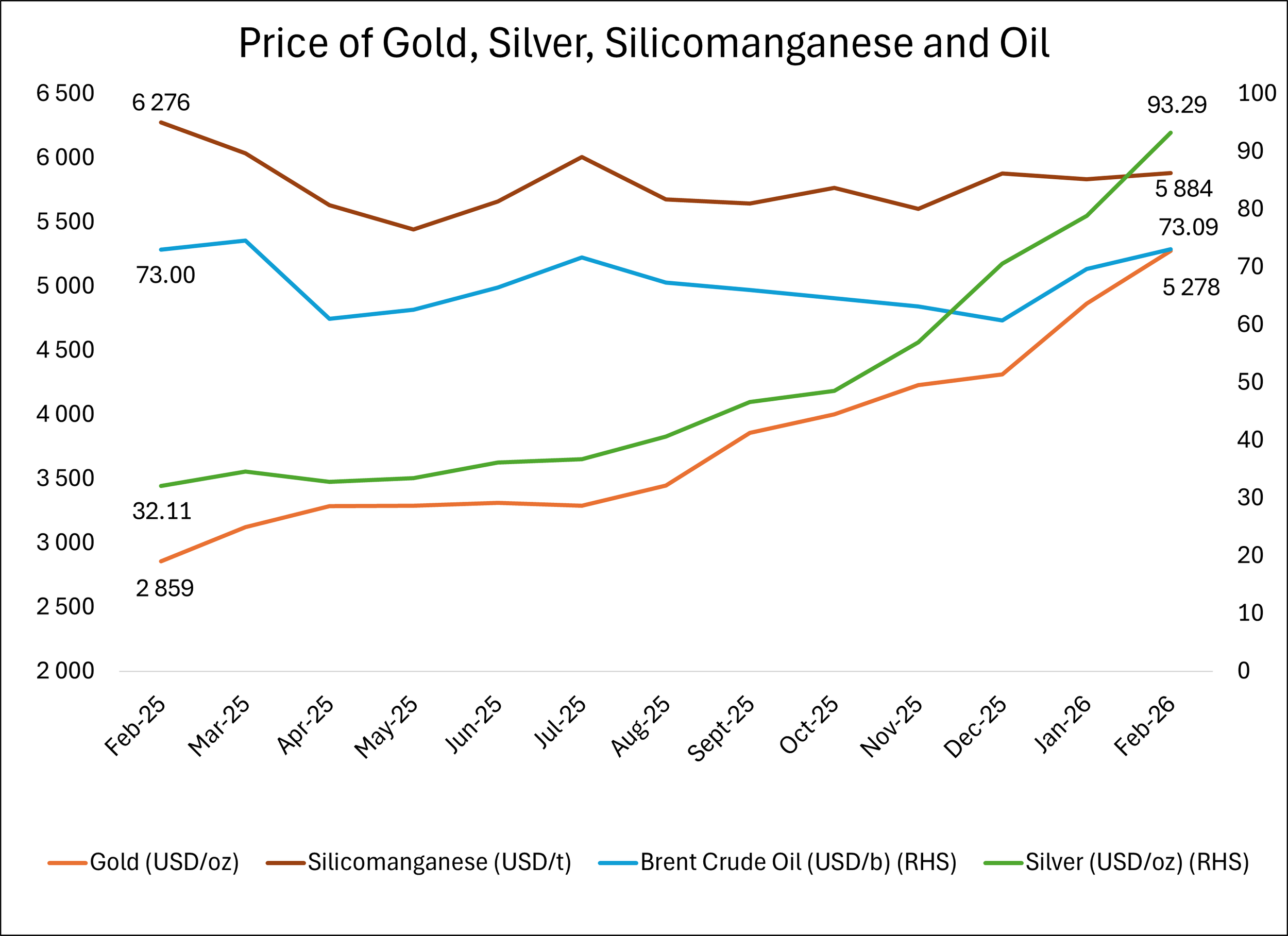

Commodities

Gold (USD/oz)

Safe haven demand

Rose during geopolitical tensions and inflation uncertainty

Gold reaffirmed its role as a portfolio hedge during uncertainty

Silver (USD/oz)

Hybrid metal

Followed gold (safe haven) and is also tied to industrial demand

More volatile than gold due to dual role (industrial + monetary)

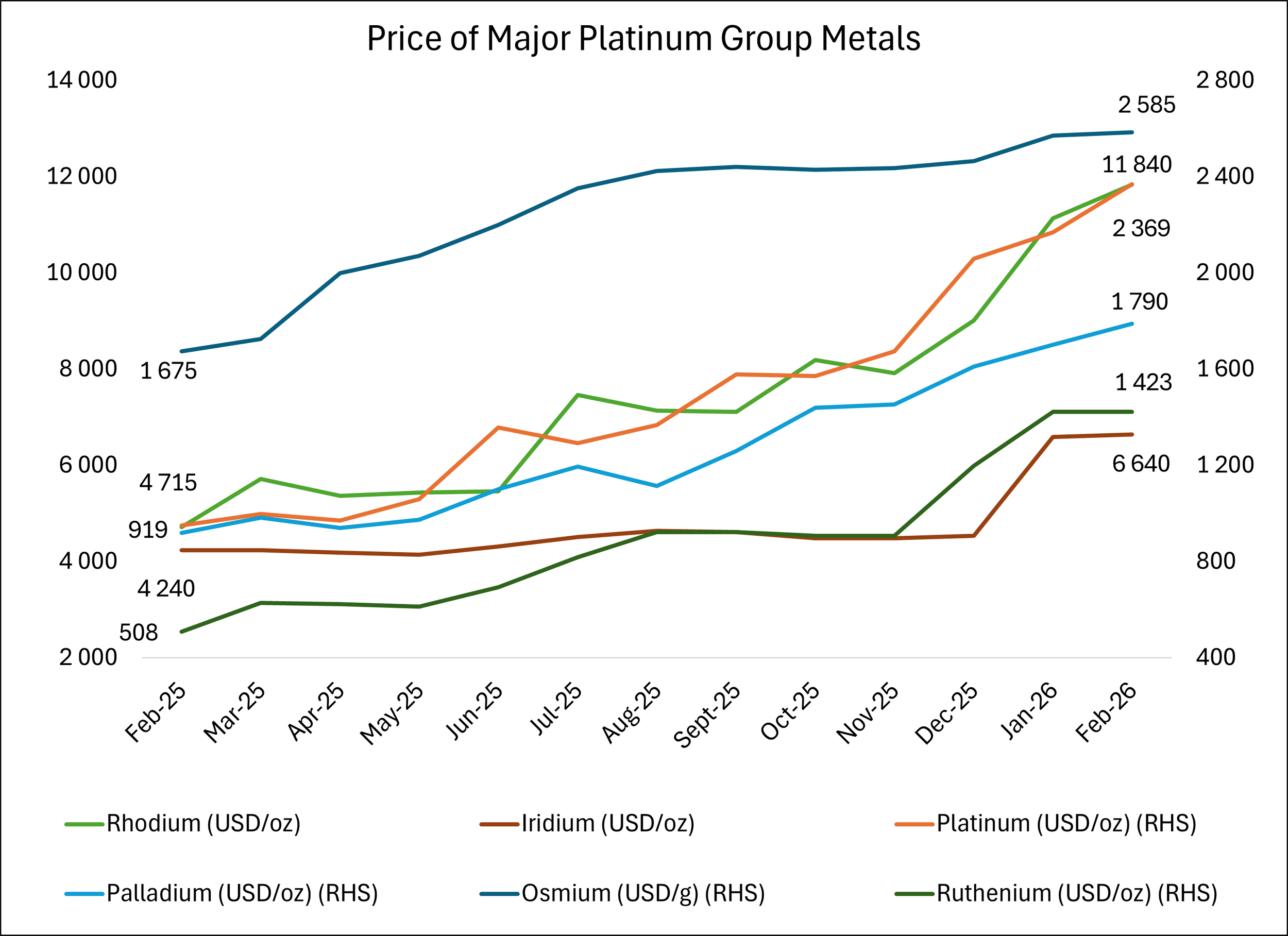

Platinum Group Metals (PGMs)

Structural pressure with cyclical support

Weakness due to EV transition reducing catalytic converter demand

Support from supply constraints and SA production dynamics

PGMs remain a structurally challenged but cyclical opportunity asset

Brent Crude Oil

Shock-driven spike

Stable in 2025 but saw a sharp spike in 2026 due to Strait of Hormuz disruption and war risk

Oil briefly surged above $110/bbl in March 2026

Energy remains the single biggest macro shock variable in global markets

Of the commodities shown, gold and silver ended February 2026 at record monthly closes, oil had a nice recovery and silicomanganese down by more than 5% Y/Y in February 2026

All the major Platinum Group Metals (PGMs) were up by over 50% Y/Y in February 2026, with rhodium the best performer and osmium the weakest

Conclusion

The 2025/26 financial year highlighted a clear shift back to macro-driven markets, where movements were influenced more by interest rates, inflation expectations, and geopolitical developments than by company fundamentals alone.

This environment reinforced the value of diversification, as different asset classes—such as commodities and South African equities—responded differently to global events, helping to manage risk and enhance returns. Market direction was largely dictated by changing policy expectations, with optimism around potential rate cuts driving gains, while uncertainty led to corrections. At the same time, geopolitics re-emerged as a key force, with war, trade tensions, and tariffs directly impacting inflation, oil prices, and currency movements.

For investors, the key takeaway is that markets are now shaped by multiple, interconnected forces—including interest rate cycles, inflation dynamics, geopolitical risks, and long-term structural shifts—making a diversified, actively managed investment approach more important than ever.

Written and compiled by Jason Mattes and Runes le Roux

Sources & References

Nedgroup Investments. (2026). Budget 2026: Encouraging signals for long-term financial planning. Available at: ttps://www.nedgroupinvestments.com/content/NGISingleSiteContent/Local/Individual-Investor/learn-more/news

Moonstone Information Refinery. (2026). Budget strengthens saving for retirement, says Sanlam. Available at: https://www.moonstone.co.za/upmedia/uploads/library

Allan Gray. (2026). 2026 Budget: A good news story. https://www.allangray.co.za/latest-insights

South African Reserve Bank (2025). Monetary Policy and Interest Rate Decisions. Available at: https://www.resbank.co.za

International Monetary Fund (2026). South Africa Economic Outlook and Policy Recommendations. Available at: https://www.imf.org

Deloitte (2025). Africa Economic Outlook. Available at: https://www.deloitte.com

Trading Economics (2025–2026). South Africa Interest Rate & Inflation Data. Available at: https://tradingeconomics.com

Associated Press (2026). Global Oil Market and Geopolitical Developments. Available at: https://apnews.com